The Role and Position of Cash in Kopernik Portfolios (May 2026)

We often receive questions about cash levels; as such we wanted to present a short whitepaper about our views on cash and its role in our portfolios. At Kopernik, we do not have cash position targets. Cash is solely a residual of our fundamental, bottom-up investment process and active investment discipline. As prices rise, making a stock more expensive, we trim our positions and cash levels go up; we then can deploy that cash when and where prices go down, making a stock more attractive.

If asked, “is cash a good thing, or a bad thing,” then the answer is “yes.” Cash is a horrible long-term investment but provides wonderful optionality as part of a disciplined valuation process. It can be viewed as a call option, one with virtually no expiration date, on every sector and geography, and with an unknown strike price from which the investor can advantageously choose. The more disciplined the investor, the more attractive the strike price. Let’s explore this further below.

Cash: A Horrible Long-Term Investment

“Paper money eventually returns to its intrinsic value: zero.”

—Voltaire

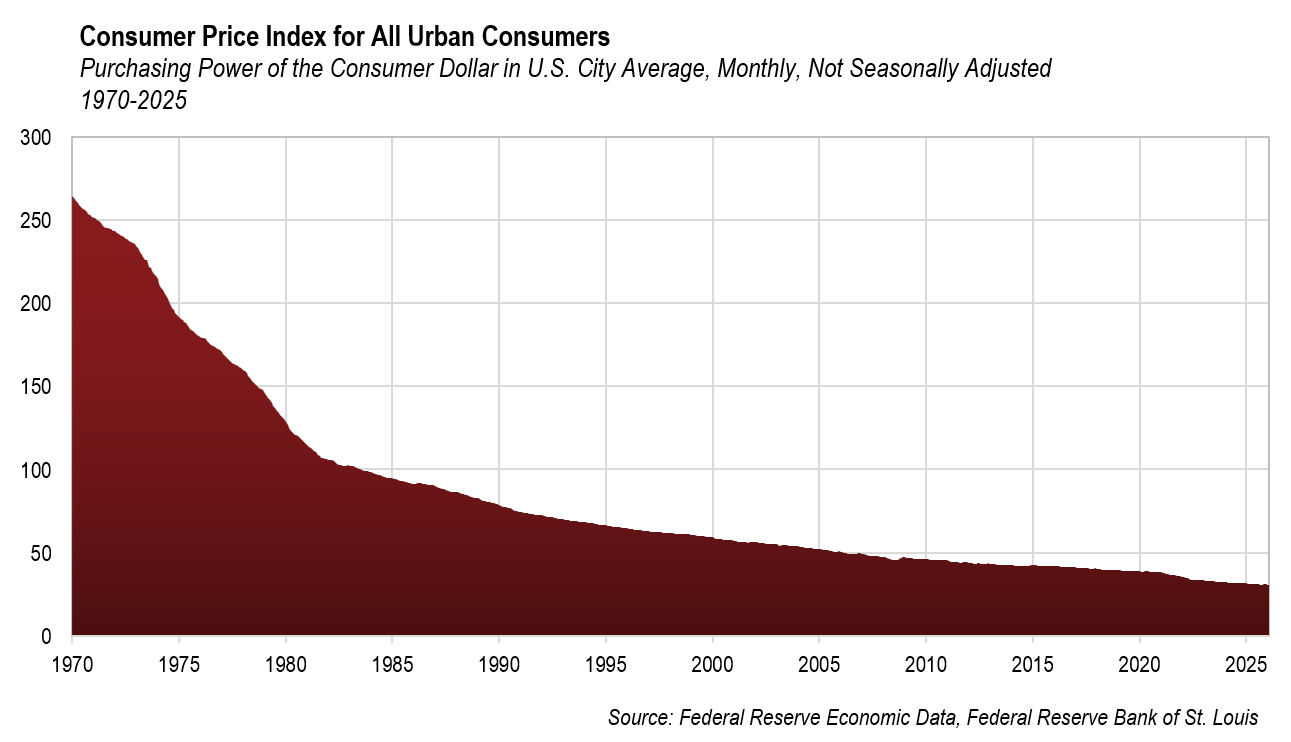

We agree cash is a terrible long-term investment in inflationary periods—one need only look to history for examples. As the chart below shows, the U.S. dollar has lost 88% of its purchasing power since 1971, when President Nixon reneged on America’s obligation to keep the dollar backed by gold. This all happened during the height of the American Empire. One can only wonder what the next 50 years will look like in these times of high debt, perpetual reckless spending, and constant government deficits.

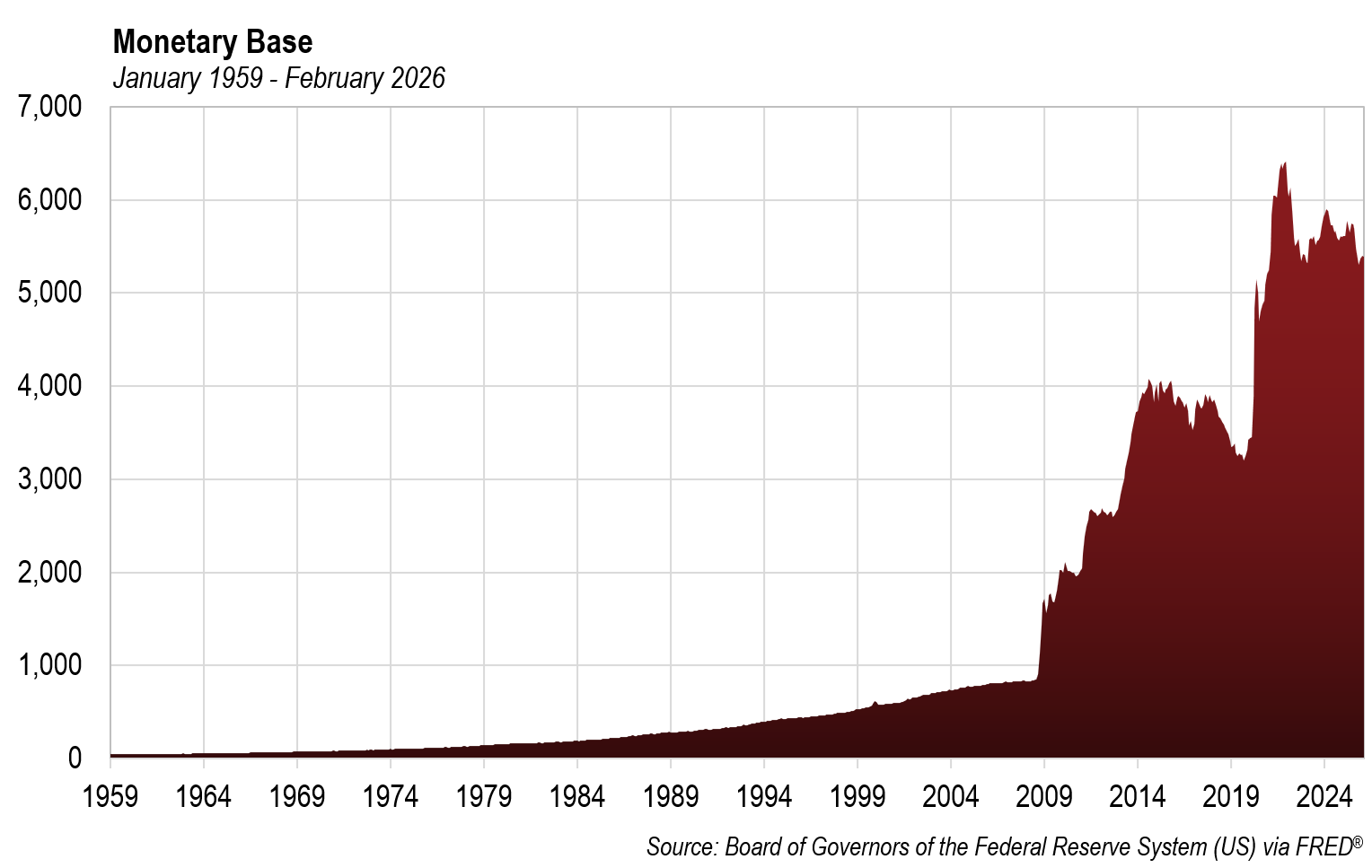

As we have argued for some time, we are in an inflationary environment today. To quote Milton Friedman, “inflation is always and everywhere a monetary phenomenon.” The U.S. monetary base is up 6.5 times since 2008, portending significant inflation in the future, if Friedman was even half right.

Jim Grant has pointed out that even at the Fed’s target rate of 2% inflation, consumer prices would go up five times during an average person’s lifetime. The Consumer Price Index (CPI) has exceeded the Fed’s target now for 60 straight months. In addition, many believe the CPI understates inflation; it’s hard to argue otherwise.

There are many examples of when money printing has gotten well out of hand. An infamous example is Weimar Germany, when the printing presses could not print money fast enough. At the height of inflation in 1923, consumers lost purchasing power within minutes; a 5,000-mark cup of coffee cost 8,000 marks by the time it was drunk. In 1922, a loaf of bread cost 160 deutschmarks; a year later, it cost 200 billion. Children would use piles of marks as building blocks and people would burn them to heat their homes. Criminals would steal a suitcase full of money, keep the bag, and leave the cash behind. The printing presses quite literally could not keep up.

Lately, it seems as though people are beginning to realize that money printing is debasement of the currency. The increase in interest in stores of value, including precious metals, illustrates that people are growing concerned about whether their cash still has value. This begs the question: if money printing debases currency, and we’ve just seen large amounts of money printing both in the U.S. and globally, then why is our cash position high. We understand why our clients might ask the question. From the perspective of many investors, high cash levels can be a drag on performance or indicate a manager asleep at the wheel and not finding new opportunities.

At Kopernik, price is paramount—and that’s the same with cash. As we take advantage of binary thought processes in the market, the question isn’t “do we like cash?” The question is “what can we get for our cash?”

Cash or Companies? Our preference changes with price.

Cash is what we use to buy things. Take, for example, a car. Say a dealer lists a Toyota Corolla for $29,000. That’s a fair price for that particular vehicle, so the difference between cash and things is negligible—the buyer is indifferent between the $29,000 in cash and the $29,000 for the Toyota Corolla. If, however, the dealership advertises a Corolla for $15,000, then the preference becomes clear—the Corolla is a much better deal; at $15,000, it might be worth it to even buy 2! But let’s take this one step further. Say we buy the Corolla, and three days later the dealership calls and said it overextended itself, needs inventory, and offers to buy our Corolla back for $40,000. At this point, all things equal, we prefer the cash to the car.

The same is true of stocks. We say frequently cash is residual to our process, but what does that actually mean in practice? It means we prefer stocks less (relative to cash) when they have run up; we trim them and take profits. This sometimes leads to higher cash balances, especially when markets perform well.

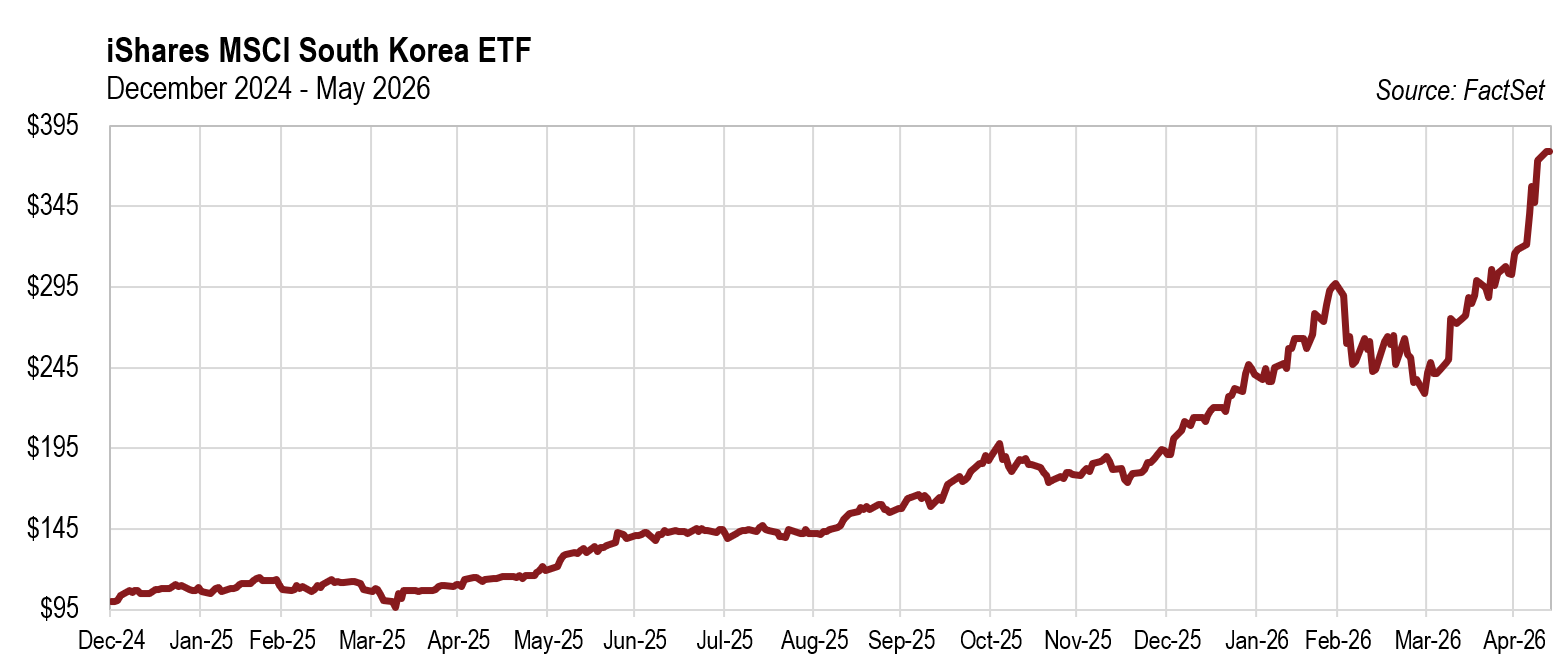

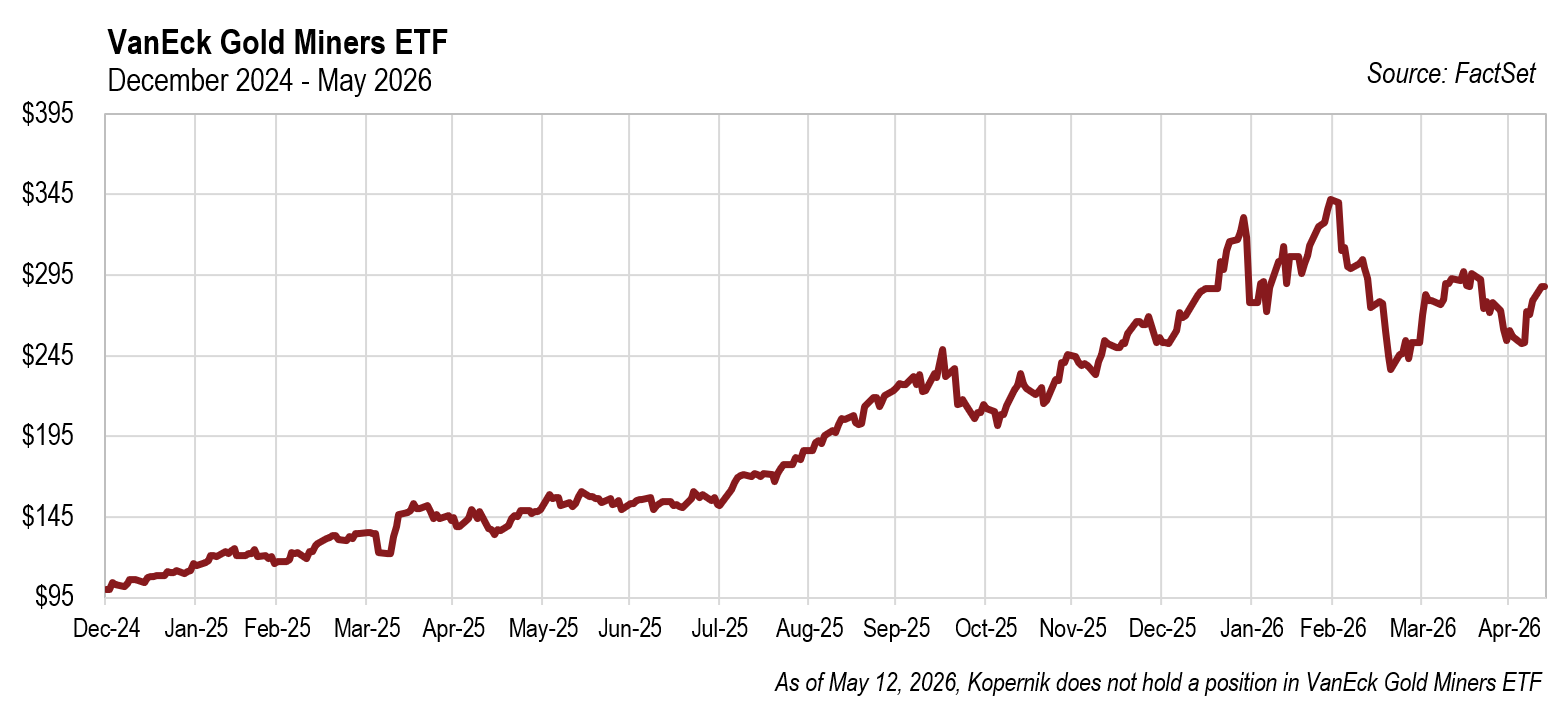

This was the case in 2025, as many areas of Kopernik’s portfolio had significant runs. Should we prefer South Korean companies more, or less, after they have rallied more than 50%? Gold miners more, or less? Platinum group metals producers more, or less?

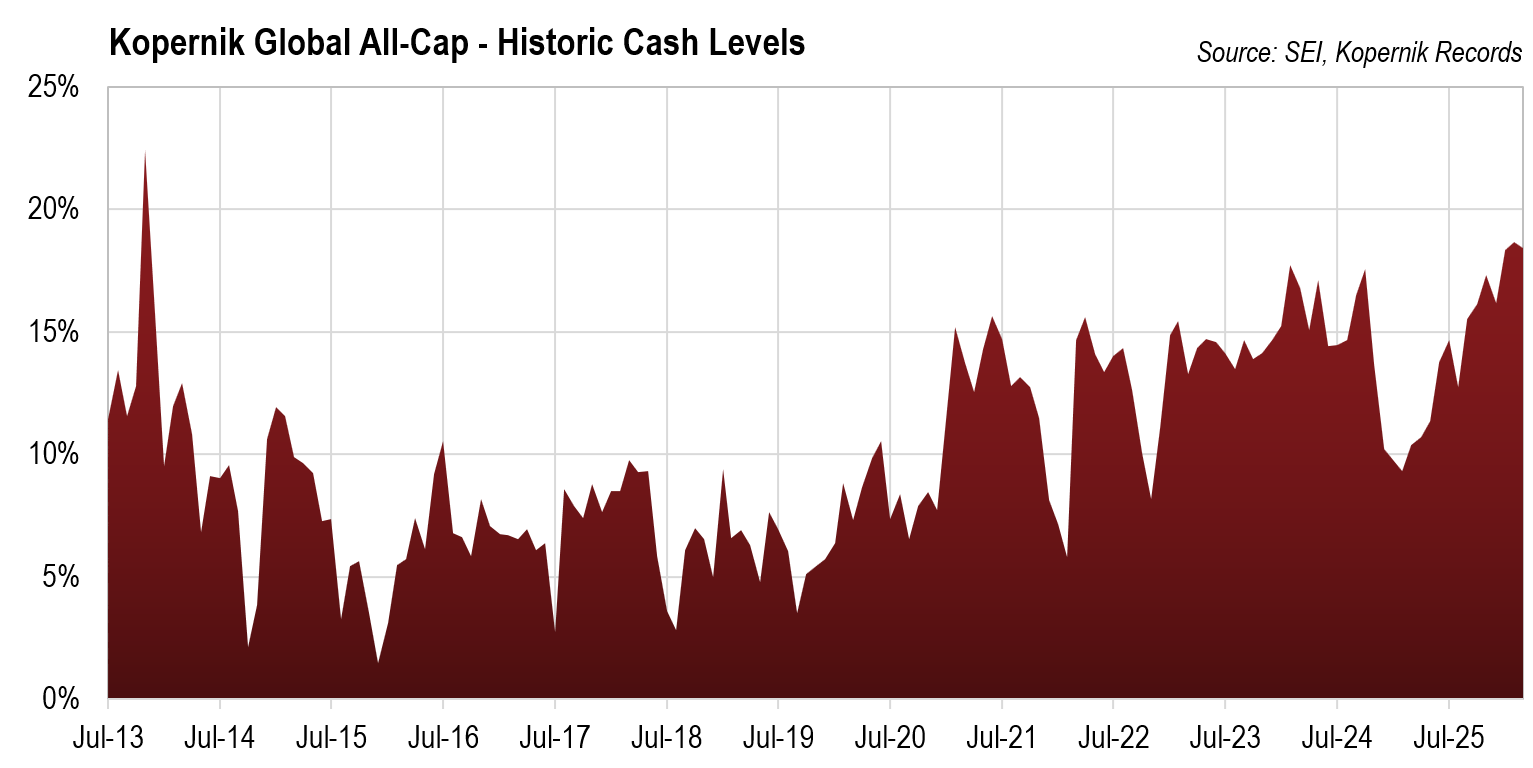

As you can see in the chart above, our cash levels have fluctuated significantly over the years. When stock prices drop, we deploy cash. Value stocks have suffered for the last decade and a half, sometimes more deeply than other times. Some of our readers may recall 2014 and 2015, two of the worst years ever to be a value investor. However, opportunities abound when stock prices fall, and our cash levels dropped precipitously as we took advantage of mispricings. Note the large drop in cash during 2015, the worst period that we can remember for value stocks. Similarly, during routs of value stocks during 2018 and 2019, cash balances dropped meaningfully. Of course, cash plunged during the Covid panic. Balances went to zero briefly, although it is hard to tell from the chart. Again, during the inexplicable plunge in resource and Korean stocks in late 2024, significant amounts of cash were put to work. The next opportunity will come soon enough.

More recently, we have seen our cash levels rise significantly. When multiple areas of the portfolio are performing well simultaneously, as happened in 2025, this leads to higher cash balances. While many of these stocks are off their highs, prices remain similar to the elevated levels of 2025 or early 2026.

A buy and hold strategy would have worked well for these stocks during 2025, but an active trimming and adding process adds significant value as well. More on this below.

Active management of the portfolio—including the residual cash—can enhance returns

Fortunately, because we are active managers, we can find places to put that cash to work. This is especially true in volatile periods (and volatile stocks!), because market volatility affords us the opportunity to buy stocks at lower prices, bargain prices. One example of this is our position in AXIA Energia SA (“AXIA”; formerly Eletrobras), Brazil’s largest electric utility. We have owned AXIA since Kopernik’s inception, and, while it has had periods of strong performance, overall, it has had unimpressive returns for the past 10 years. Yet due to our disciplined trimming and adding process, it is the best performing stock in the Global All-Cap portfolio over the last dozen years.1

Other examples include uranium, where we were several years too early but were able to use cash to keep averaging down and maximize our position at the bottom. We were fortunate our thesis did eventually play out and we did very well, even including the lean years. Properly managed volatility is an active manager’s friend. In current markets, with valuations stretching to new all-time highs, volatility should be expected. Even during rising markets, trimming and adding to volatile stocks has added meaningful value relative to a buy and hold strategy.

“You’re deluding yourself if you believe your stocks, however cheap they are, won’t temporarily go down when Mr. Market decides to correct. When that happens, your cash becomes ammunition for future bargains.”

—Charles de Vaulx

What do we prefer to cash?

Fiat currency is a good medium for transactions, but a poor store of value. We like assets which are needed and are relatively scarce. When we say “things,” this is to what we are referring. To sum up and oversimplify: when things are cheap, we prefer them to cash, and we buy them. When things are expensive, we are happy to trade our things for cash and redeploy it to other things which are, in our analysis, inexpensive relative to the cash. With strong performance in 2025, it isn’t a surprise that the cash balances in Kopernik’s portfolios trended higher. “Things” had gotten expensive—especially in several large parts of the portfolio, including South Korean stocks and gold miners. We trimmed back our positions in areas which had run up, and our cash balances rose accordingly.

Yet it also shouldn’t be a surprise that we refuse to rest on our laurels. Our team of sector-specialist analysts is constantly evaluating new, undervalued opportunities. As such, we are finding many areas to invest, several of which are detailed below. Given the current era of volatility, and barring another large run-up by the market, it is reasonable to assume cash levels will come down.

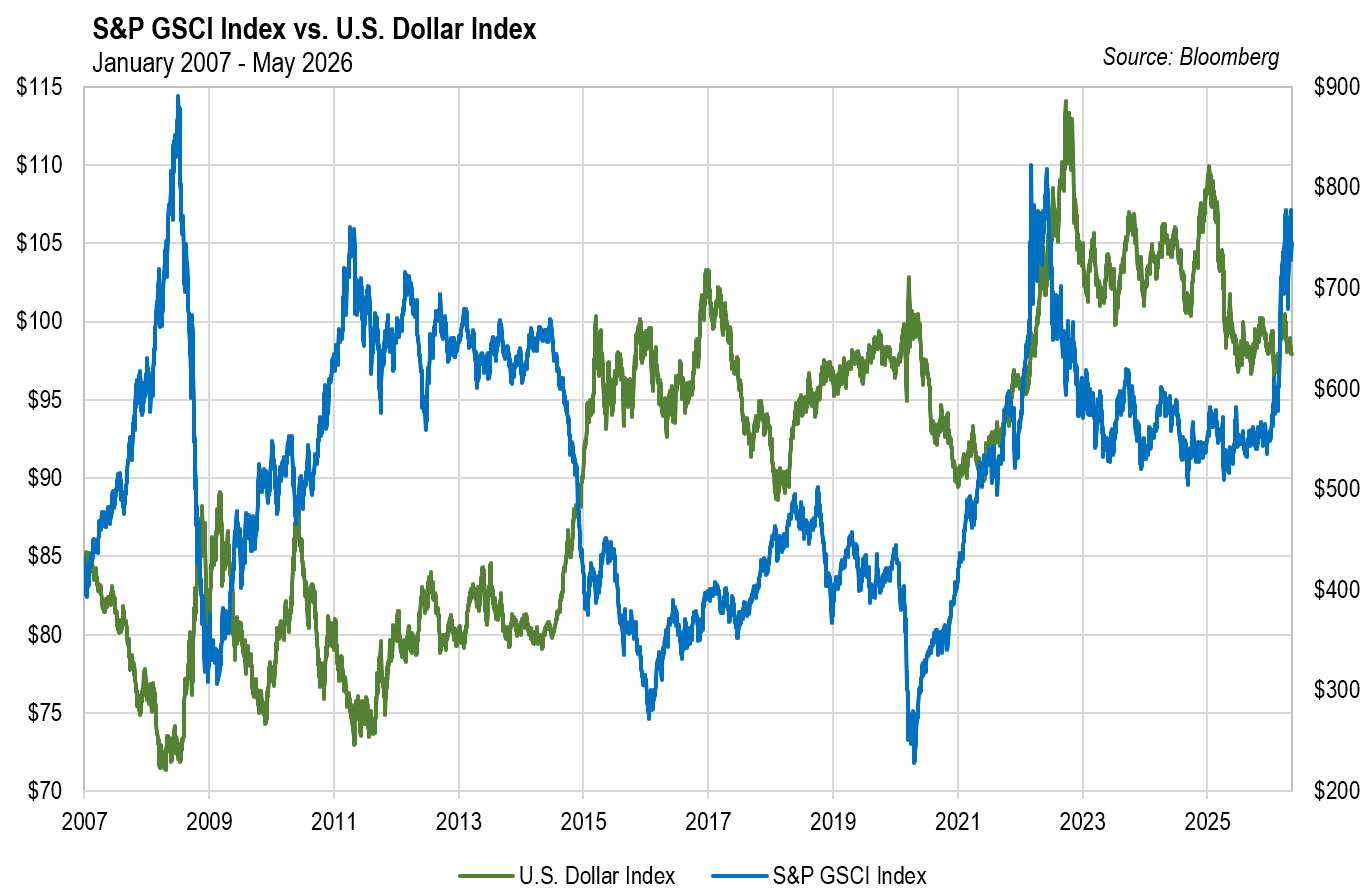

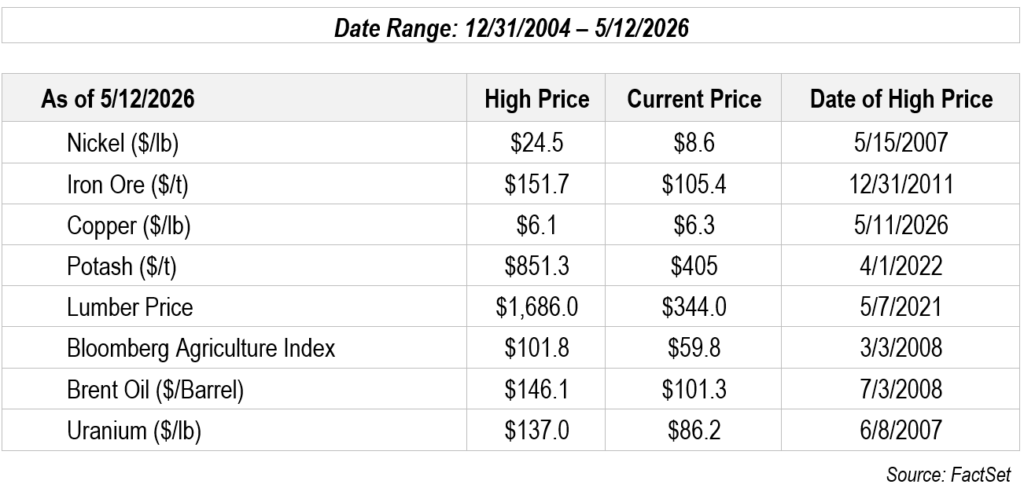

Before signing off, let’s touch on some of the places where we have been deploying cash. The chart below shows the extent to which commodities have languished over the past couple of decades in dollar terms. Notice we are finding value in a wide range of commodities, not just in gold.

Commodities

For many years now, commodities have made up a significant portion of our portfolio. It has surprised us that assets which are needed and scarce have been unpopular among investors, but the fact they have been out of favor has provided many opportunities. The same is true today. Over the course of 2025, the spot price of gold and the stock prices of gold miners went up significantly. As we trimmed back our gold positions, we have redeployed the cash generated into other areas where we see more upside, including base and industrial metals, timber, and energy. Many commodity prices are well off their highs, and we are once again taking advantage of the opportunity. In our opinion, nearly 2 decades of profligate money printing and undisciplined monetary policy cannot possibly be neutral. Inflation is likely to flow into commodities. We are fond of quoting seventeenth-century Irish-French economist Richard Cantillon: “The river, which runs and winds about in its bed, will not flow with double the speed when the amount of water is doubled.”

Prices like these suggest that, while the Cantillon wave seems to have buoyed gold, inflation has not yet flowed into other commodities. It is an opportune time to buy, in our opinion.

International Conglomerates

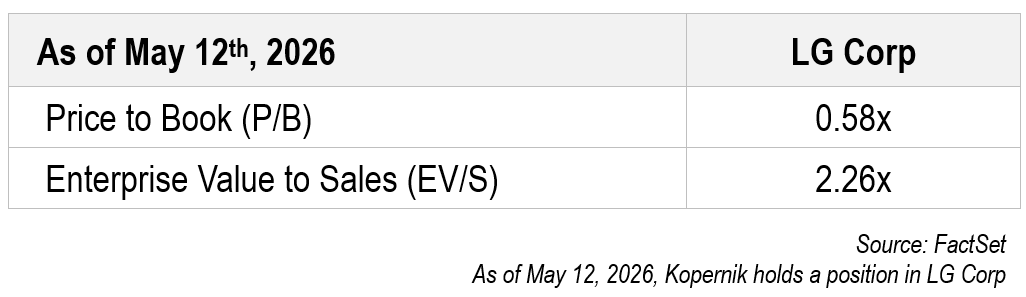

As we wrote early in 2025, “Conglomerates are portfolios of businesses which should be evaluated on their own individual merits. Recent investor proclivity to lump them all together and affix a negative connotation has created an exciting investment opportunity for those who are willing to do the requisite fundamental analysis.” This remains true in 2026. Many conglomerates, especially in emerging markets, trade below book value. Within conglomerates, one of our larger positions is in LG Corp, which trades at a significant discount to our sum-of-the-parts valuation: one could buy LG Chem, LG Health, LG Uplus, and LG Electronics in the market, or, with the willingness to put in the hard work to analyze a complex company, could buy the parent company for a 65% discount.

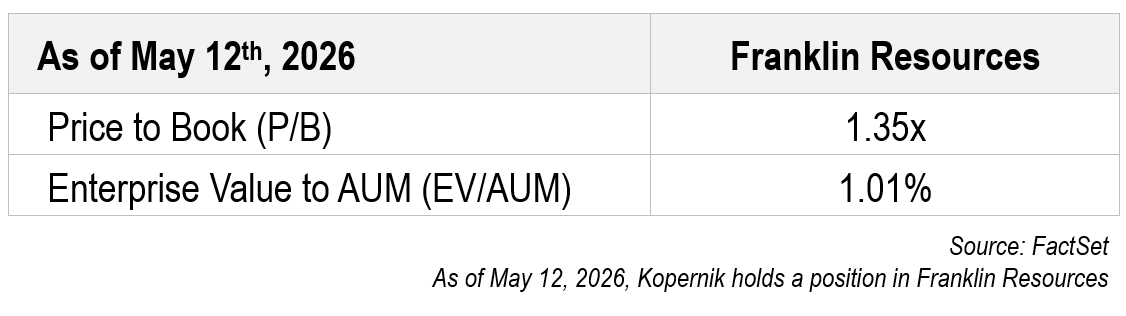

Asset Managers

Many asset managers are trading below 1% of their AUM. In our opinion, it is reasonable for asset managers to trade around 2.5% of their AUM. Franklin Resources Inc. is a strong franchise which currently trades at extremely depressed multiples.

U.S. Healthcare

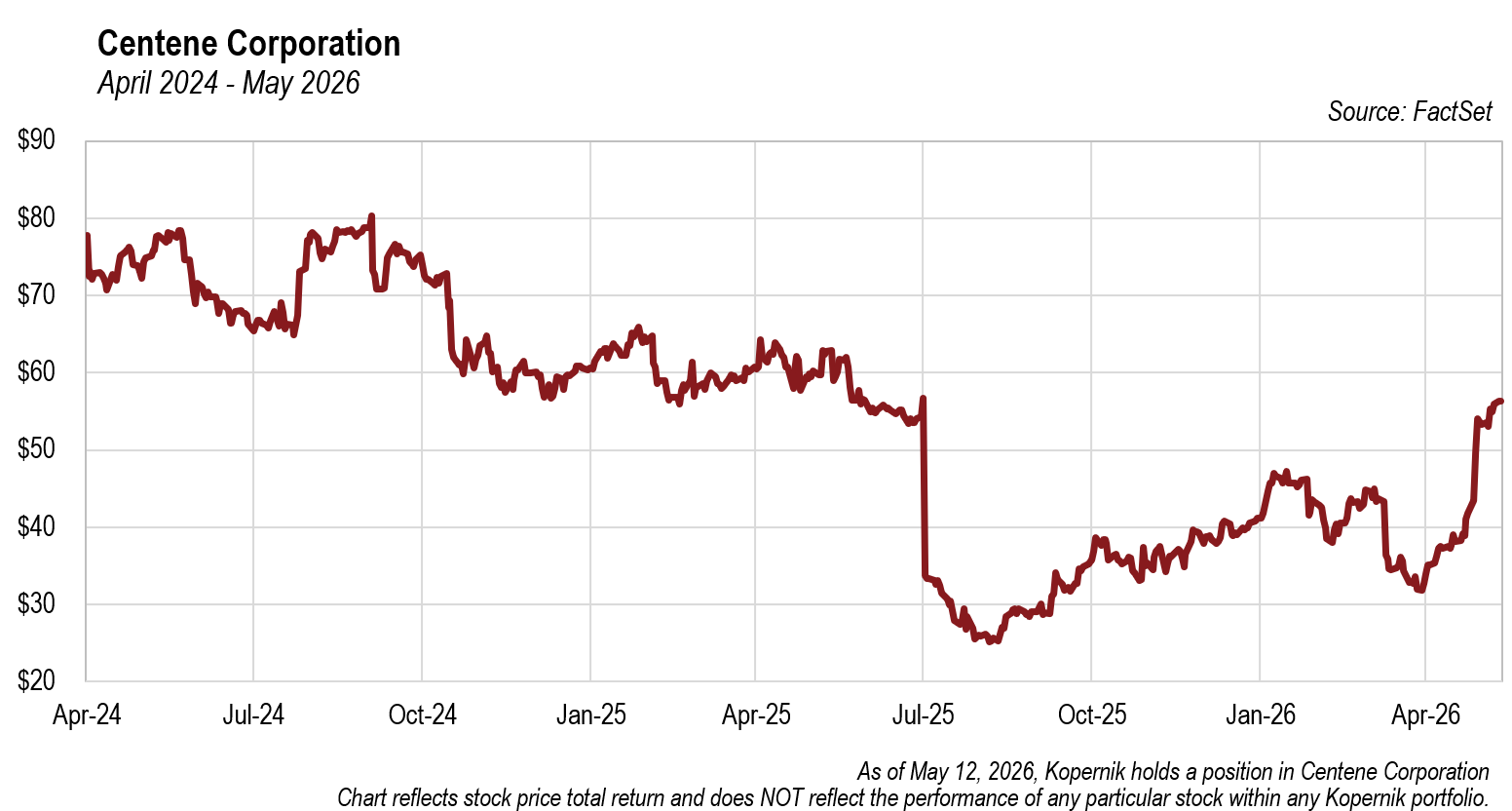

We have also seen some opportunities in U.S. healthcare. Centene Corporation and Molina Healthcare Inc. are two Medicaid managed care organizations whose stock prices collapsed last year. We took advantage and added both companies to the portfolio. Recent volatility has allowed us to trim our exposure. It is worth noting that if current volatility continues, the weighting in various sectors will likely rise and fall as opportunities present themselves.

Conclusion

Cash is a residual to our very disciplined investment process. We don’t believe it is the right approach for investors to be fully invested at all times. Rather, we let the prices of stocks dictate whether or not we’re interested in using that cash to buy them. We agree cash is a horrible long-term investment, but we have also shown it provides wonderful optionality in the short term. It can help returns, especially during bouts of volatility, which, as equity investors, we should be expecting.

Investors often hold cash at the worst times. They hold too much cash at the bottom of the cycle when they’re fearful, and they often hold too little cash at the top of the cycle when they feel the pressure to be fully invested. While our cash levels are more elevated, we still have more than 80% of Kopernik portfolios invested in very high-quality companies and trading at extremely attractive levels. We have a history of putting cash to work when opportunities arrive, and we are hopeful the current volatility will continue giving us chances to invest more of this cash soon.

As always, thank you for your support.

Kopernik Investment Research Team

May 2026

- Based on the holdings of a fully seasoned representative account. Performance results of the total portfolio available upon request. ↩︎

Definitions

Consumer Price Index (CPI) – is a key economic indicator measuring the average change over time in prices paid by consumers for a representative basket of goods and services, often used to gauge inflation.

iShares MSCI South Korea ETF – The fund is a free float-adjusted market capitalization-weighted index that is designed to measure the performance of the large- and mid-capitalization segments of the equity market in Korea.

Van Eck Gold Miners ETF (GDX®) – seeks to replicate as closely as possible, before fees and expenses, the price and yield performance of the NYSE Arca Gold Miners Index (GDMNTR), which is intended to track the overall performance of companies involved in the gold mining industry.

S&P GSCI Index – is a premier benchmark for investment in global commodity markets, tracking the performance of 24 exchange-traded futures contracts across energy, industrial metals, agricultural products, livestock, and precious metals.

US Dollar Index – measures the value of the U.S. dollar relative to a weighted basket of six major foreign currencies: the Euro (EUR), Japanese Yen (JPY), British Pound (GBP), Canadian Dollar (CAD), Swedish Krona (SEK), and Swiss Franc (CHF). It acts as a key indicator of the dollar’s overall strength.

Bloomberg Agricultural Subindex – is a commodity group subindex of the Bloomberg Commodity Index (BCOM). It is composed of futures contracts on coffee, corn, cotton, soybeans, soybean oil, soybean meal, sugar and wheat. It reflects the return of underlying commodity futures price movements only and is quoted in USD.

Important Information and Disclosures

The information presented herein is proprietary to Kopernik Global Investors, LLC. This material is not to be reproduced in whole or in part or used for any purpose except as authorized by Kopernik Global Investors, LLC. This material is for informational purposes only and should not be regarded as a recommendation or an offer to buy or sell any product or service to which this information may relate.

This letter may contain forward-looking statements. Use of words such was “believe”, “intend”, “expect”, anticipate”, “project”, “estimate”, “predict”, “is confident”, “has confidence” and similar expressions are intended to identify forward-looking statements. Forward-looking statements are not historical facts and are based on current observations, beliefs, assumptions, expectations, estimates, and projections. Forward-looking statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control and are difficult to predict. As a result, actual results could differ materially from those expressed, implied or forecasted in the forward-looking statements.

Please consider all risks carefully before investing. Investments in a Kopernik strategy are subject to certain risks such as market, investment style, interest rate, deflation, and illiquidity risk. Investments in small and mid-capitalization companies also involve greater risk and portfolio price volatility than investments in larger capitalization stocks. Investing in non-U.S. markets, including emerging and frontier markets, involves certain additional risks, including potential currency fluctuations and controls, restrictions on foreign investments, less governmental supervision and regulation, less liquidity, less disclosure, and the potential for market volatility, expropriation, confiscatory taxation, and social, economic and political instability. Investments in energy and natural resources companies are especially affected by developments in the commodities markets, the supply of and demand for specific resources, raw materials, products and services, the price of oil and gas, exploration and production spending, government regulation, economic conditions, international political developments, energy conservation efforts and the success of exploration projects.

Investing involves risk, including possible loss of principal. There can be no assurance that a strategy will achieve its stated objectives. Equity funds are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus. Investments in foreign securities may underperform and may be more volatile than comparable U.S. securities because of the risks involving foreign economies and markets, foreign political systems, foreign regulatory standards, foreign currencies and taxes. Investments in foreign and emerging markets present additional risks, such as increased volatility and lower trading volume.

The holdings discussed in this piece should not be considered recommendations to purchase or sell a particular security. It should not be assumed that securities bought or sold in the future will be profitable or will equal the performance of the securities in this portfolio. Current and future portfolio holdings are subject to risk.

Commodities may be affected by changes in overall market movements, changes in interest rates, and other factors such as weather, disease, embargoes, or political and regulatory developments, such as trading activity of speculators and arbitrageurs in the commodities. Investing in commodities entails significant risk and is not appropriate for all investors.

To determine if a Kopernik Mutual Fund is an appropriate investment for you, carefully consider the Fund’s investment objectives, risk factors, charges and expenses before investing. This and other information can be found in the Fund offering materials, which may be obtained by contacting your investment professional or calling Kopernik Mutual Fund at 1-855-887-4KGI (4544). Read the offering materials carefully before investing or sending money. Check with your investment professional to determine if a Kopernik Mutual Fund is available for sale within their firm. Not all funds are available for sale at all firms.