Bayou Jubilee (Jun 2026)

“Bayou Jubilee” is a song by The Nitty Gritty Dirt Band (also known as the Dirt Band or NGDB), a band that has been around since 1966 but continues to play together. They are probably best known for their cover of Jerry Jeff Walker’s “Mr. Bojangles” and “Fishin’ In the Dark,” which reached #1 on the Country charts. Will the Circle be Unbroken (volumes I, II, and III), collaborative albums, became cult classics. My personal favorite is probably “Ripplin’ Waters.” Their cover of Hank Williams’ song “Jambalaya” is excellent. I’m also a fan of “Face on the Cutting Room Floor.” Per Genius, “It contrasts a woman’s rosy childhood visions of LA red carpets with the gritty reality of signing with a shady agent, getting exploited, and ultimately catching the 2:30 train out of town while the studio replaces her with ‘so many more’.” Many decades later, it might be updated from LA actresses to D.C. Cabinet members 😉.

I was fortunate to see NGDB live, but not in their prime. Returning to our title song:

“Nothing in this world such a pure delight

As a fais-do-do on a Saturday night

Work your tail off all week long

But forget about your troubles with a party and a song”

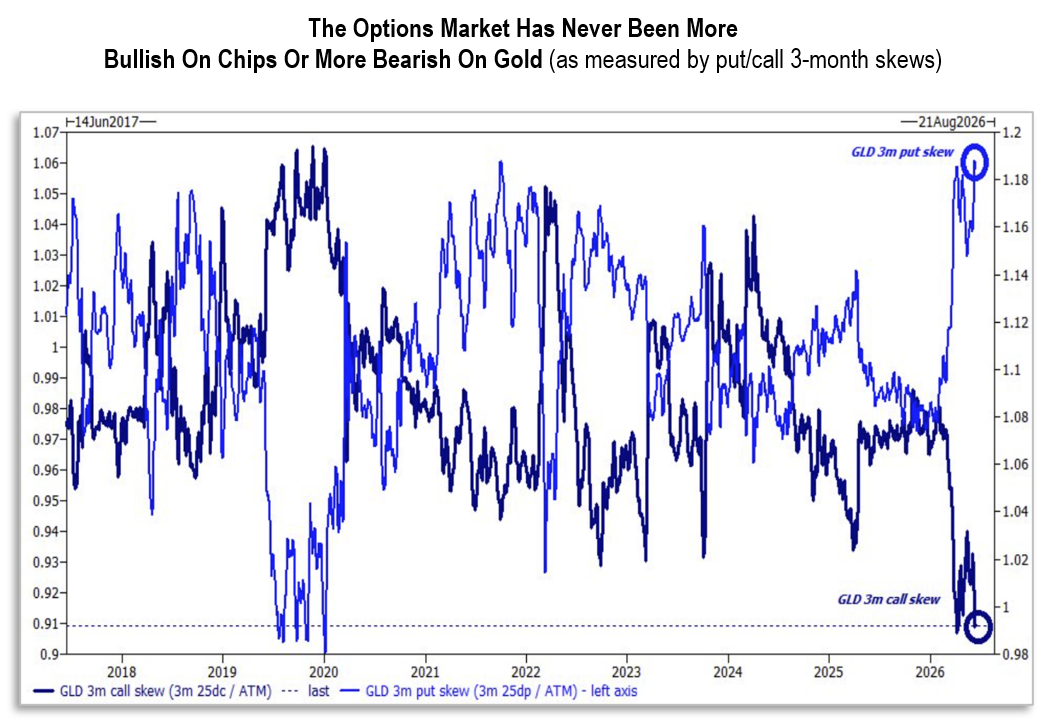

As the lyrics suggest, when times are tough, often a little music and a party are just what the doctor ordered. And nowadays, with rising inflation, rising interest rates, expensive energy, massive debt levels, shockingly high budget deficits adding to that debt, alarming geopolitical conflict, and faith in institutions at all-time lows, Wall Street’s solution – Party. Fais do-do! Jubilation. The mood is captured by the chart below.

Market cap to GDP, said to be Warren Buffett’s favorite measure, is at an all-time high, approaching four times its level of two decades ago. Market cap is also at an all-time high as measured relative to book value, revenues, replacement value, and CAPE (cyclically adjusted price to earnings). Fais do-do indeed. Jubilee!

“Dancin’ so hot you’d think their shoes were burning

Grandma’s in the corner shakin’ it too

She’s got her own version of a Cajun boogaloo

Get out the fiddle rosin up the bow

There’s gonna be some music and I hope it ain’t slow

Grab your baby dance ’til three down at the Bayou Jubilee.”

— NGDB

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.”

— Chuck Prince, Former Chairman & CEO of Citigroup

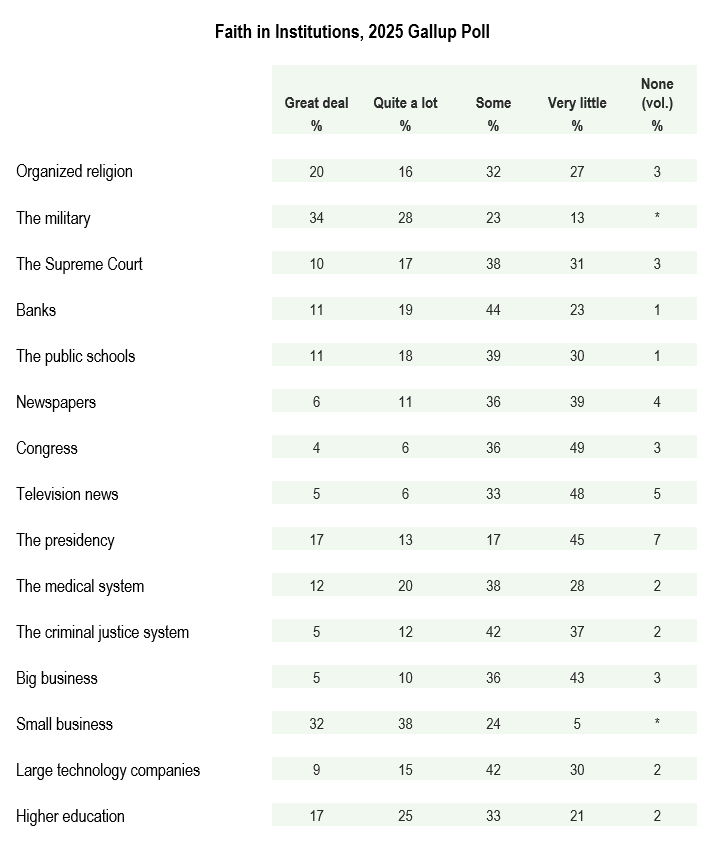

Usually, when the markets are jubilant, the overall environment is extremely supportive. Yet here we are with record challenges. In the appendix is a chart of the sorry state of low esteem in which major institutions are currently held. The chart doesn’t capture how much lower these numbers are relative to the past. It’s been quite a plunge. Quite a conundrum, trying to reconcile the markets to their underlying fundamentals. But rest assured, the stock market is not the topic at hand. Many gifted prognosticators have recently written persuasive arguments on the markets; some are quite constructive while others are predictive of doom and gloom. We have nothing worth adding to the discourse.

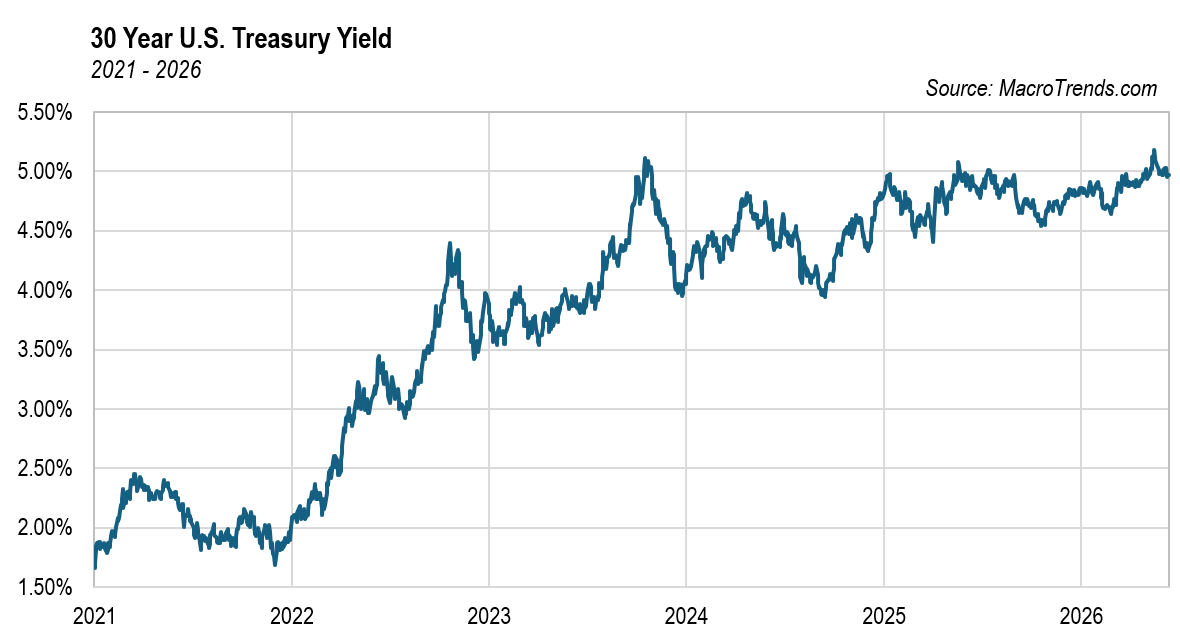

Our topic is “Jubilees.” Thus far we’ve focused on one definition, a grand celebration, often commemorating an important milestone. 2021 commemorated a major milestone, the 40th anniversary, and likely end of the bull market in U.S. Treasuries. Coincidentally, the 40th anniversary is typically called the Ruby Anniversary, and perhaps fittingly, the bond market has been a sea of red since then.

This factoid provides a good segue to the type of jubilee that is pertinent here – a debt jubilee: a large-scale cancellation or forgiveness of debts. To provide background, here is some narrative from a website of Lyn Alden:

“Debt Jubilees: a 4,000+ Year History

In ancient times, debts were often about crop harvest outcomes. Farmers would rack up tabs with various counterparties throughout the year and pay them off at harvest season, but if the harvest failed for one reason or another, the farmers would be financially destroyed. When they were unable to pay their debts, they would generally lose their land to their creditors, and if that didn’t cover it, they might be forced into slavery to their creditors for a period of time.

If that happens enough times to enough people, it eventually becomes destabilizing at the whole societal level rather than just the individual level. More and more people end up as landless slaves, and wealth concentrates more and more into the hands of the few. The numbers get very lopsided, and eventually those with nothing to lose, and who greatly outnumber their masters, resort to violent revolution. No king wants to be in power when that happens.

So, kings would often use decrees to forgive certain types of debt and servitude, restoring freedom or land and resetting things for another several decades. Or they would put limits on how many years someone could be a debt slave until they are freed, even if their time in slavery doesn’t fully cover their debts.

Debt jubilees date back at least 4,000 years to ancient Sumer, Babylon, and other areas of western Asia. Ancient kings would sometimes forgive societal debts as a matter of public stability, and some of them put the practice into law at regular intervals or triggered by certain catalysts.

Ancient Israelites had the concept of a debt jubilee every five decades, where people could come out of servitude, return to their land, and so forth.

Solon, who is credited for building some of the foundations of ancient Greek democracy in the sixth century BC, used a partial debt jubilee as part of his solution to avoid catastrophic class conflict.”

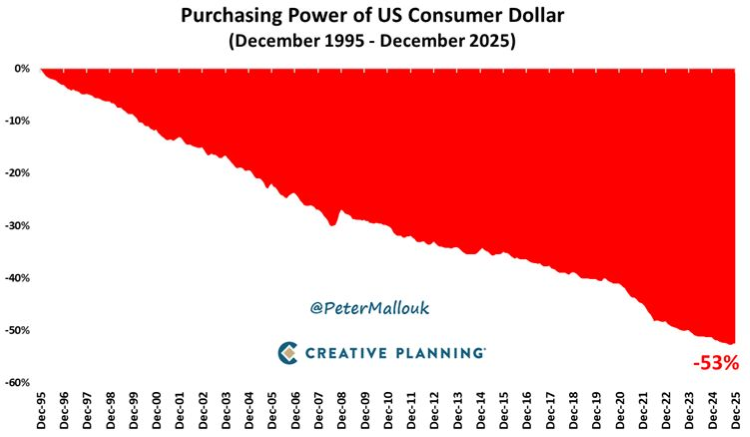

So it’s clear that debt jubilees have both a long history and a purpose. Is this ancient history relevant today? It’s often said, what can’t go on forever won’t go on forever. The current debt-orgy certainly can’t. Similarly, what can’t be repaid, won’t be repaid. It is clear that the U.S. government, and most all the others, have no intention of getting their fiscal houses in order. Even if they did, history shows that current debt levels are not manageable. Now, when we say it won’t be repaid, we mean repaid with something of equivalent economic value to what was lent. Paying back 2026 dollars with 2056 dollars is quite likely. The chance that 2056 will have anywhere near the same purchasing power as 2026 dollars is inconceivable. This chart shows the loss of purchasing power of the US dollar, which has more than halved over the past 30 years.

Certainly, the next 30 years will be much worse given the comfort level the government has with perpetual $2 trillion deficits. Over the past century, the dollar has lost over 99.5% of its value relative to gold. It would be shocking if the next century isn’t much worse (if such a thing is possible). Devaluation is said to be endemic to all systems, especially democracies. Scottish historian Alexander Fraser Tytler was correct, “democracies can only last until the voters discover that they can vote themselves largesse from the public treasury.”

While inflation continues to erode the value of dollars, there are other worrisome signs for debt holders. During this millennium to date, we’ve witnessed increasing signs of politics trumping rule of law. At various times, mortgages have been forgiven, and student loans and rents have been deferred. LME (liability management exercises) have become commonplace. (Time doesn’t permit a discussion of these travesties so you may want to google them or read Jim Grant’s many great discussions on the topic.) Certainly, in the overdone private credit arena, the increasing usage of gates in recent months (a gate provision allows fund managers to limit or halt investor withdrawals during redemption periods) suggests a reallocation of wealth is underway. When times get tough, the powers that be do what they feel they must. As for the rest of us, Caveat Emptor.

Before moving on, let’s return to Ms. Alden:

“It wasn’t necessarily out of kindness that rulers did this (although a significant subset of them aged well in history and were wise); it was basically just a solution to a societal math problem. It’s like if you run a computer long enough, eventually it starts to work less efficiently. As memory leaks and other issues build up, it starts to freeze and slowdown, frustratingly. It’s a mildly unstable system in other words. Refreshing the power and rebooting the system gets the computer running smoothly again.

Debt jubilees generally served that purpose: an occasional reset to wipe out some of the growing instabilities from prior generations, and begin with a cleaner slate and a renewed social contract. Otherwise these societal imbalances tend to cleanse themselves with more violent revolutions, with the many poor vs the few rich.”

We’ve painted a picture that is not rosy, more of a ruby-red, a scarlet warning signal. Not to worry. While we’ll make no effort to downplay the seriousness of the challenges, we’ll also present the case that a little joy is still in order.

Obviously, long-term bonds are not exciting. They arguably yield less than real inflation and certainly don’t offer an attractive return, even sans a jubilee. In the 1980s, long rates approached 15% and short rates reached 22% during a time when the economic challenges were minuscule in relation to today. And don’t look here for encouragement on the U.S. stock market. After all, the market is at record valuations based upon almost every relevant metric and signs of speculation are rife. SpaceX just came public at 100 times revenues and immediately jumped 23%. Trillions of dollars are being poured into price-agnostic funds. That’s not at all what the “efficient market hypothesis” hypothesizes. To appropriate one of Jim Grant’s former sayings about the bond market, “you’ll find better values in your hotel minibar than you will in the S&P 500 index.”

Fortunately, there is much merit to the old cliché, “it’s not a stock market but a market of stocks.” Breaking things down to first principles (for what it’s worth – “nitty-gritty” refers to the core, essential, or practical details of a situation or task. It strips away high-level overviews and gets down to the fundamental facts), stock ownership is ownership of an underlying business. Nobody should invest money in a stock without making every effort to understand and appraise the value of that business. While that is always a truism, fundamental analysis is now more important than ever. Why? The dollar and other currencies are losing value and seem destined to continue doing so. The index is teeming with “ticking timebombs.” Dynamics are changing rapidly. Society’s “safety nets” are shaky. The onus is increasingly on individuals and institutions to create and defend the purchasing power of their businesses and portfolios.

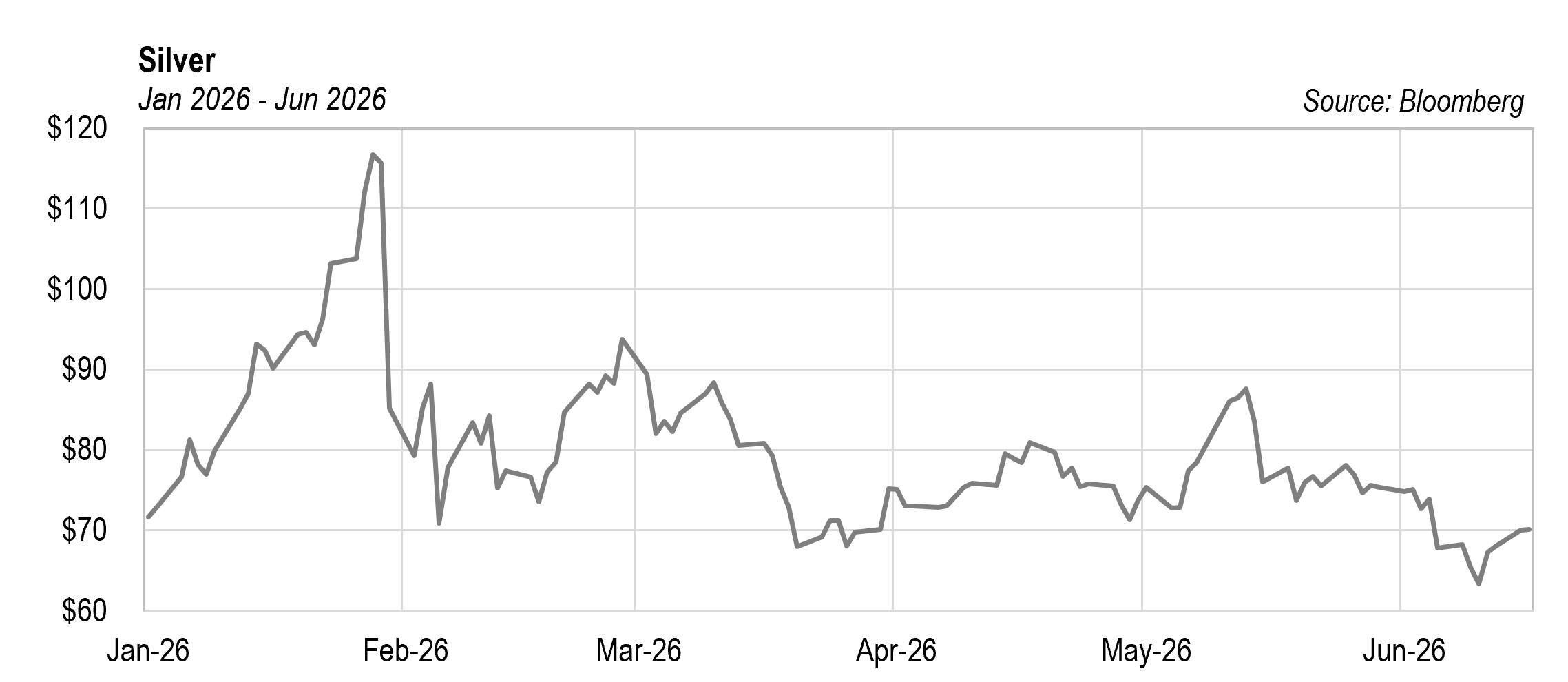

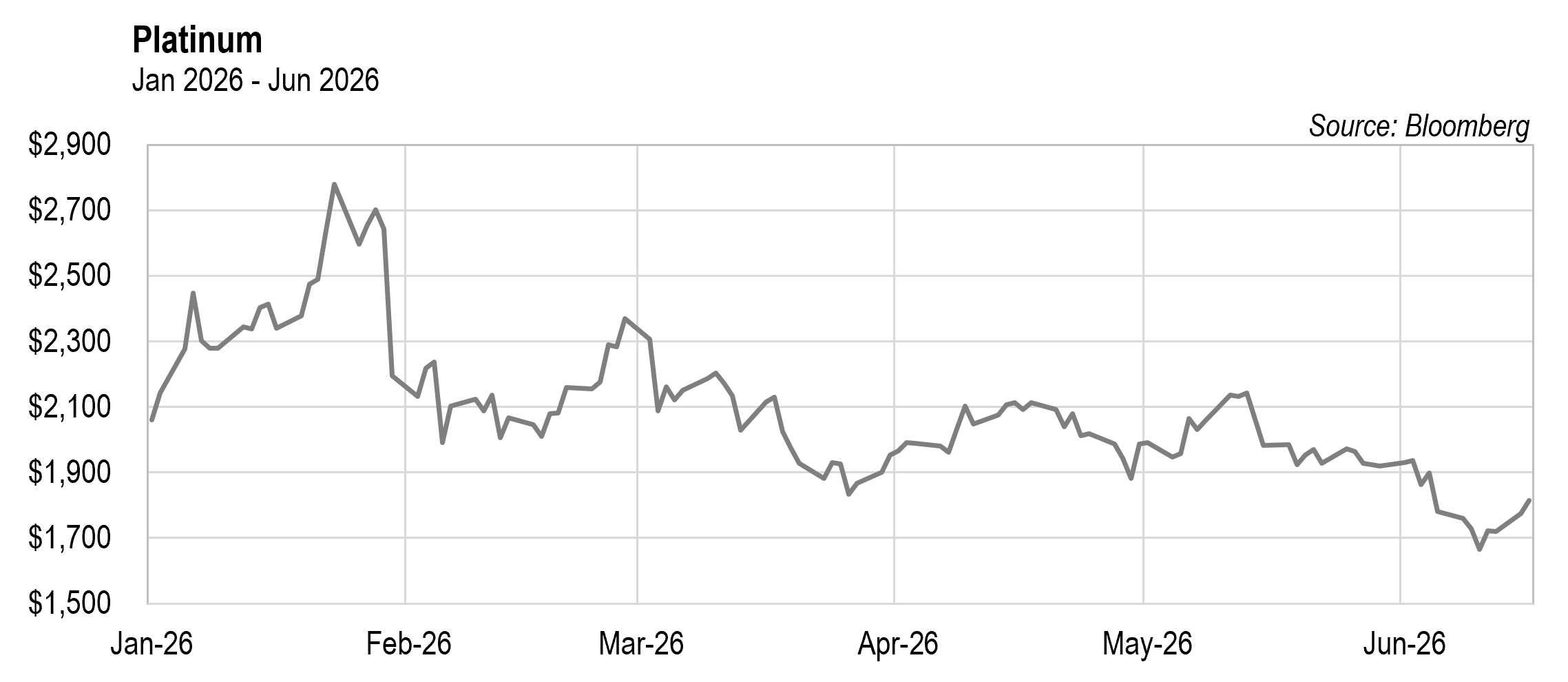

While the explosive return of manic market conditions has been concerning, in many ways it’s also been a godsend. As anointed theme stocks soared, well-known and proven stores of value have corrected back to interesting levels. Valuable, needed, hard-to-replicate assets and franchises such as cell networks, railroads, natural gas reserves, and resources such as gold, silver, platinum, uranium, and other metals are all at meaningful discounts to their prior levels. We are now able to repurchase some of the gold mining stocks that we sold earlier this year. Since the end of January 2026, gold is down 22%. Over that same period, the GDX ETF is down over 30% and GDXJ is down 35%. We’ve been able to add to Royal Gold at a 28% discount to its recent past; International Tower Hill looks great at a near 40% discount to February; Novagold stock is down 45% from where we were trimming the position four months ago. While our gold mining positions came down substantially, platinum miner positions, post significant sales, remained at a high single-digit position. We’ve been happily adding back to Valterra, Impala, and Sibanye at 40%, 50%, and 50% discounts to recent highs, respectively.1

Elsewhere in resources, there have been substantial corrections in uranium, natural gas, many agricultural commodities, and select quality stocks. For example, Ivanhoe Mines is down 55% from earlier this year.2

Railroads are a much-needed and very hard-to-replicate industry. Hong Kong-based Guangshen Rail is down 62% from its levels from almost two decades ago. Amazing. It’s less than 10x earnings and ½ of book value. Likewise, West Japan Rail sits at just over half of its pre-COVID level. It’s less than 10x earnings and around book value. Tokyo Metro hasn’t been publicly traded for that long, but still is down almost a third from last year’s level. It trades at 12x earnings and a 25% premium to book value. Tokyo Metro reported 2.5 billion passengers last year; West Japan Rail reported 1.9 billion. Guangshen is smaller and only operates between Guangzhou and Shenzhen; even so, it still had over 63 million passengers in 2025. These railroads may be undervalued, but they are clearly not worthless.3

We always (semi) joke that many people would rather give up food than their cell phone service. Following a 35% correction, Chile’s dominant phone provider Entel resides in the bargain bin, trading at less than 6x earnings and 56% of book value. Korea Telecom is a third below February’s level and sits at 8x earnings and three-quarters of book value.4 The conglomerates that we’ve featured over the past several years such as CK Hutchison, GS Holdings, and LG Corp, have performed well, but still all sit at less than half of book value.5 Furthermore, book value is well understated in our opinion. Many other sectors are also on our radar screen, but this sampler should suffice to make the point.

Before signing off, it’s important to point out that outside of technology, the market is well into correction/bear market territory. There are bargains in the making.

Looking for safer, more attractive investment opportunities unfortunately requires changing direction, possibly feeling some pain. For value stocks, it shouldn’t be jubilee but joyful resurrection. In the words of Tom Fogerty (John’s late brother):

“Have you heard (have you heard) of the joyful resurrection?

A way to bring your mind back from the dead

Have you heard (have you heard) of the joyful pain direction?

Change of scene is gonna change your head”

The brothers’ former group Creedence Clearwater Revival, long a favorite of mine, fits in well with our Cajun/bayou motif. They’ve been called the Kings of Swamp Rock. At any rate, the tech stocks may prove to be the real thing and go up from here; prove to be the real thing but get thumped like the real deals from the past (Canals, Rails, Telecom and Radio, Semiconductors, Internet stocks, all of which fell more than 75%); or they could prove to have been over-hyped. Others can play that speculation game. True investors should roll up their sleeves, perform due diligence, and buy undervalued companies. Jean-Marie Eveillard points out that value investing is pain. The “pain direction” may be the requirement to participate in the “joyful resurrection” of value stocks. Advice to passive investors who zombie-like, toss their money into overvalued indices: perhaps a little investment analysis is a good “way to bring your mind back from the dead…A change of scene is gonna change your head.”

The bifurcation in the market is extreme, which is encouraging for active managers, who can unearth undervalued gems in this otherwise very expensive market. History suggests the pain will soon move from value managers to momentum managers. A change of scene is in order. We continue to patiently anticipate the coming chapters of this ongoing market saga.

Cheers,

David B. Iben, CFA

Co-Chief Investment Officer & Lead Portfolio Manager

June 2026

Never Ending Story

The futures is now: Michael Selig, chair of the Commodity Futures Trading Commission, took to CNBC Monday to explain his agency’s rationale in approving perpetual futures contracts for U.S. punters on May 29.

The products – listed derivatives featuring no expiration date nor ownership of the underlying asset – have quickly caught on stateside, with Kalshi revealing last Thursday that it handled $3 billion in trading volume during a beta testing period which lasted just over a week. “We’re going to make sure there’s proper disclosure,” Selig said, “and, to the extent that there’s questions about suitability, the brokers have to make those calls and make sure they’re evaluating the customers that are trading in their markets.”

One prominent industry player emphatically dissents from the CFTC’s verdict. On June 4, CME Group CEO Terry Duffy deemed the so-called perps a “disaster waiting to happen,” pointing to outsized degrees on leverage on offer, which reached 50:1 on some venues as of early this month. “I believe the [capital markets have] been supplanted by the speculation market, and that does not suit anyone’s interest,” he added.

To be sure, perps present a competitive threat to the venerable, 128-year-old bourse, with CME shares down 14% over the past month. Last Thursday, CME announced it will offer 24/7 trading contracts in crude oil futures beginning June 30, with Bloomberg reporting a day later that the CFTC may block that initiative, owing to concerns that off-market trading could aggravate market volatility in today’s geopolitically fraught backdrop.

Regulatory snafus and all, perps have already carved out a niche in Wall Street’s speculative vehicle du jour: punters traded more than $1.2 billion of SpaceX perps on last Friday’s IPO date via the Hyperliquid platform and $5.6 billion on Binance, with that combined tally equating to roughly one-tenth the dollar-equivalent turnover on the Nasdaq.

With Elon Musk’s rocket maker opting to initially float just over 4% of outstanding shares, perps arguably contribute to price discovery, though not without growing pains. SPCX shares closed for regular trading on Monday at a $2.5 trillion market cap, with that valuation lurching to $3 trillion on Hyperliquid a few hours later. Bloomberg reports that a sharp increase in funding rates for bearish bets initiated a “classic short squeeze,” spurring more than $50 million in short position liquidations Monday evening, per data from Coinglass. SpaceX wrapped up today’s cash session with a $2.64 trillion market cap.

A Monday press release, meanwhile, illustrated the category’s latest round of financial innovation, albeit one slightly outside the Graham-and-Dodd investing curriculum. Yesterday, the Bittam Exchange trumpeted the debut of crypto perps, dangling a $300 bonus for newly registered users alongside some noteworthy features:

No [know-your customer rules], instant trading – start trading within seconds without complicated verification;

Up to 200x leverage – meet diverse trading strategies for both beginners and pros;

Source: Almost Daily Grant’s, June 16, 2026.

Boy I love those old time tunes

They can tickle your senses like a Cajun moon

Creole food sure tastes fine

When you wash it on down with that homemade wine

Get out the fiddle rosin up the bow

There’s gonna be some music and I hope it ain’t slow

Grab your baby dance ’til three down at the Bayou Jubilee

Grab your baby dance ’til three down at the Bayou Jubilee

There’s Pierre and his girl Laverne

Dancin’ so hot you’d think their shoes were burning

Grandma’s in the corner shakin’ it too

She’s got her own version of a Cajun boogaloo

Get out the fiddle rosin up the bow

There’s gonna be some music and I hope it ain’t slow

Grab your baby dance ’til three down at the Bayou Jubilee

Grab your baby dance ’til three down at the Bayou Jubilee

Nitty Gritty Dirt Band, “Bayou Jubilee”

Important Information and Disclosures

The information presented herein is proprietary to Kopernik Global Investors, LLC. This material is not to be reproduced in whole or in part or used for any purpose except as authorized by Kopernik Global Investors, LLC. This material is for informational purposes only and should not be regarded as a recommendation or an offer to buy or sell any product or service to which this information may relate.

This letter may contain forward-looking statements. Use of words such was “believe”, “intend”, “expect”, anticipate”, “project”, “estimate”, “predict”, “is confident”, “has confidence” and similar expressions are intended to identify forward-looking statements. Forward-looking statements are not historical facts and are based on current observations, beliefs, assumptions, expectations, estimates, and projections. Forward-looking statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control and are difficult to predict. As a result, actual results could differ materially from those expressed, implied or forecasted in the forward-looking statements.

Please consider all risks carefully before investing. Investments discussed are subject to certain risks such as market, investment style, interest rate, deflation, and illiquidity risk. Investments in small and mid-capitalization companies also involve greater risk and portfolio price volatility than investments in larger capitalization stocks. Investing in non-U.S. markets, including emerging and frontier markets, involves certain additional risks, including potential currency fluctuations and controls, restrictions on foreign investments, less governmental supervision and regulation, less liquidity, less disclosure, and the potential for market volatility, expropriation, confiscatory taxation, and social, economic and political instability. Investments in energy and natural resources companies are especially affected by developments in the commodities markets, the supply of and demand for specific resources, raw materials, products and services, the price of oil and gas, exploration and production spending, government regulation, economic conditions, international political developments, energy conservation efforts and the success of exploration projects.

Investing involves risk, including possible loss of principal. There can be no assurance that a strategy will achieve its stated objectives. Equity funds are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus. Investments in foreign securities may underperform and may be more volatile than comparable U.S. securities because of the risks involving foreign economies and markets, foreign political systems, foreign regulatory standards, foreign currencies and taxes. Investments in foreign and emerging markets present additional risks, such as increased volatility and lower trading volume.

The holdings and topics discussed in this piece should not be considered recommendations to purchase or sell a particular security. It should not be assumed that securities bought or sold in the future will be profitable or will equal the performance of the securities in this portfolio. Kopernik and its clients as well as its related persons may (but do not necessarily) have financial interests in securities, issuers, or assets that are discussed. Current and future portfolio holdings are subject to risk.

Commodities may be affected by changes in overall market movements, changes in interest rates, and other factors such as weather, disease, embargoes, or political and regulatory developments, such as trading activity of speculators and arbitrageurs in the commodities. Investing in commodities entails significant risk and is not appropriate for all investors.

- Royal Gold Inc.; International Tower Hill Mines; Novagold Resources Inc.; Valterra Platinum Ltd.; Impala Platinum Holdings Ltd.; Sibanye Stillwater Ltd. ↩︎

- Ivanhoe Mines Ltd. ↩︎

- Guangshen Railway Co Ltd.; Tokyo Metro Co Ltd.; West Japan Railway Co. ↩︎

- Empresa Nacional de Telecomunicaciones SA; KT Corp ↩︎

- CK Hutchison Holdings Ltd.; GS Holdings Corp. ↩︎