Oil & Gas

A conversation with energy analyst Stephen Rosenthal, CFA

What is the most important takeaway for investors in the current oil and gas market?

A defining feature of today’s oil and gas market is geopolitical disruption. Prior to recent events, the market was expected to remain modestly oversupplied. That assumption has changed materially in the near term.

The roughly 20% of the world’s oil (20 million barrels per day) that passes through the Strait of Hormuz has essentially been shut out. While there are alternative routes, these are de minimus compared to the supply disruption. Much of the Middle Eastern oil goes to Asia, where we have seen prices of end products like gasoline and jet fuel skyrocket. Uncertainty and volatility continue, and the geopolitical situation is precarious.

What is more important to us, however, is the fact that, while spot prices have responded quickly in the short term, over the long term, prices remain too low to sustain production given natural depletion rates and rising costs.

What are the key long-term risks to the industry?

A primary long-term risk is demand displacement. Breakthroughs in battery technology could materially improve the economics of renewable energy by addressing storage constraints. Nuclear power is another area to monitor. If deployment accelerates meaningfully, that could pose a risk to the oil & gas industry.

While these outcomes are plausible, they remain extremely uncertain and currently are insufficient to meet rising energy demand. The “death of oil” has been predicted for many years, but it does not seem like that’s possible in the current environment, at least not for many years to come.

| Rather than reacting to headlines, we focus on long-term fundamentals and the price required to incentivize supply. |

How do oil and natural gas fundamentals differ right now?

Natural gas markets are experiencing a more pronounced (and prolonged) geographic dislocation than oil. Prices in Europe and Asia have been substantially higher than in the U.S. for many years. Qatar supplies 20% of the global gas market; the QatarEnergy CEO recently suggested that 17% of the country’s production capacity has been taken offline for the next 5 years due to the fighting. This has driven prices even higher in Europe and Asia; by contrast, U.S. natural gas prices have remained relatively stable.

If gas in Europe and Asia is materially more expensive than gas in the U.S., over the long term, that gap should narrow, with economics accruing to low-cost producers that can access global markets. U.S. companies, such as portfolio holdings Range Resources Inc. and Expand Energy Corp., which have long-lived reserves and a low cost basis, have operating leverage to higher prices, in our opinion.

What does this environment tell us about long term energy security and supply?

Energy security has re-emerged as a central issue, particularly for regions without domestic supply. Oil and gas production naturally declines by roughly 5–8% per year without sustained reinvestment. Even flat demand requires continuous capital spending.

Periods of underinvestment tend to resolve through higher prices, as supply tightness eventually emerges. This structural reality places long-term support under energy prices, regardless of short-term volatility or political intervention.

Where do you see opportunity—and how does this fit Kopernik’s approach?

Opportunities exist in energy, but selectivity and discipline are essential. Many energy equities moved higher ahead of commodity prices, driven largely by capital rotation rather than fundamental improvement. In such environments, patience matters more than momentum.

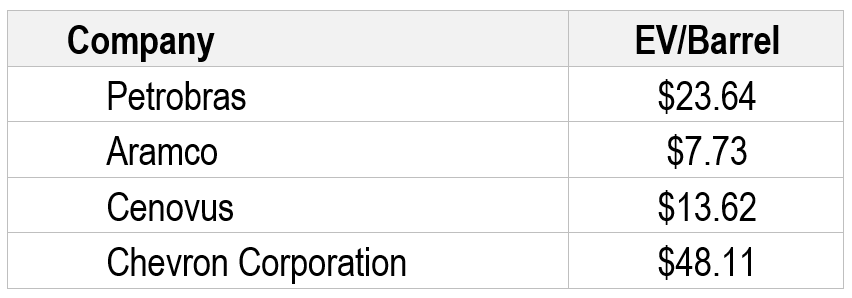

Our oil & gas holdings, including Petroleo Brasileiro SA (“Petrobras”), Saudi Arabian Oil Co (“Aramco”), and Cenovus Energy Inc (“Cenovus”), are undervalued on an enterprise value/barrel of proved reserves basis relative to many of their peers. Each company has idiosyncratic risks, but each also has a significant, long-duration asset base and low production costs.

Source: FactSet

At Kopernik, we do not invest based on short-term price movements or attempt to forecast geopolitical outcomes. Instead, we focus on identifying businesses that trade at meaningful discounts to our estimate of their risk adjusted intrinsic value. That often means maintaining our positions through volatility when fundamentals remain intact or waiting for prices to reconnect with underlying value.

Rather than reacting to headlines, we continue to apply a disciplined, bottom-up investment process grounded in valuation, margin of safety, and long-term fundamentals.

| Discipline and patience remain central to our investment approach, particularly in volatile markets. |

Important Information and Disclosures

The information presented herein is proprietary to Kopernik Global Investors, LLC. This material is not to be reproduced in whole or in part or used for any purpose except as authorized by Kopernik Global Investors, LLC. This material is for informational purposes only and should not be regarded as a recommendation or an offer to buy or sell any product or service to which this information may relate.

This letter may contain forward-looking statements. Use of words such was “believe”, “intend”, “expect”, anticipate”, “project”, “estimate”, “predict”, “is confident”, “has confidence” and similar expressions are intended to identify forward-looking statements. Forward-looking statements are not historical facts and are based on current observations, beliefs, assumptions, expectations, estimates, and projections. Forward-looking statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control and are difficult to predict. As a result, actual results could differ materially from those expressed, implied or forecasted in the forward-looking statements.

Please consider all risks carefully before investing. Investments in a Kopernik strategy are subject to certain risks such as market, investment style, interest rate, deflation, and illiquidity risk. Investments in small and mid-capitalization companies also involve greater risk and portfolio price volatility than investments in larger capitalization stocks. Investing in non-U.S. markets, including emerging and frontier markets, involves certain additional risks, including potential currency fluctuations and controls, restrictions on foreign investments, less governmental supervision and regulation, less liquidity, less disclosure, and the potential for market volatility, expropriation, confiscatory taxation, and social, economic and political instability. Investments in energy and natural resources companies are especially affected by developments in the commodities markets, the supply of and demand for specific resources, raw materials, products and services, the price of oil and gas, exploration and production spending, government regulation, economic conditions, international political developments, energy conservation efforts and the success of exploration projects.

Investing involves risk, including possible loss of principal. There can be no assurance that a strategy will achieve its stated objectives. Equity funds are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus. Investments in foreign securities may underperform and may be more volatile than comparable U.S. securities because of the risks involving foreign economies and markets, foreign political systems, foreign regulatory standards, foreign currencies and taxes. Investments in foreign and emerging markets present additional risks, such as increased volatility and lower trading volume.

The holdings discussed in this piece should not be considered recommendations to purchase or sell a particular security. It should not be assumed that securities bought or sold in the future will be profitable or will equal the performance of the securities in this portfolio. Current and future portfolio holdings are subject to risk.

Commodities may be affected by changes in overall market movements, changes in interest rates, and other factors such as weather, disease, embargoes, or political and regulatory developments, such as trading activity of speculators and arbitrageurs in the commodities. Investing in commodities entails significant risk and is not appropriate for all investors.

To determine if a Kopernik Mutual Fund is an appropriate investment for you, carefully consider the Fund’s investment objectives, risk factors, charges and expenses before investing. This and other information can be found in the Fund offering materials, which may be obtained by contacting your investment professional or calling Kopernik Mutual Fund at 1-855-887-4KGI (4544). Read the offering materials carefully before investing or sending money. Check with your investment professional to determine if a Kopernik Mutual Fund is available for sale within their firm. Not all funds are available for sale at all firms.